Baby Apparel 2030

-

Home

-

Baby Apparel 2030

International Market Scenario

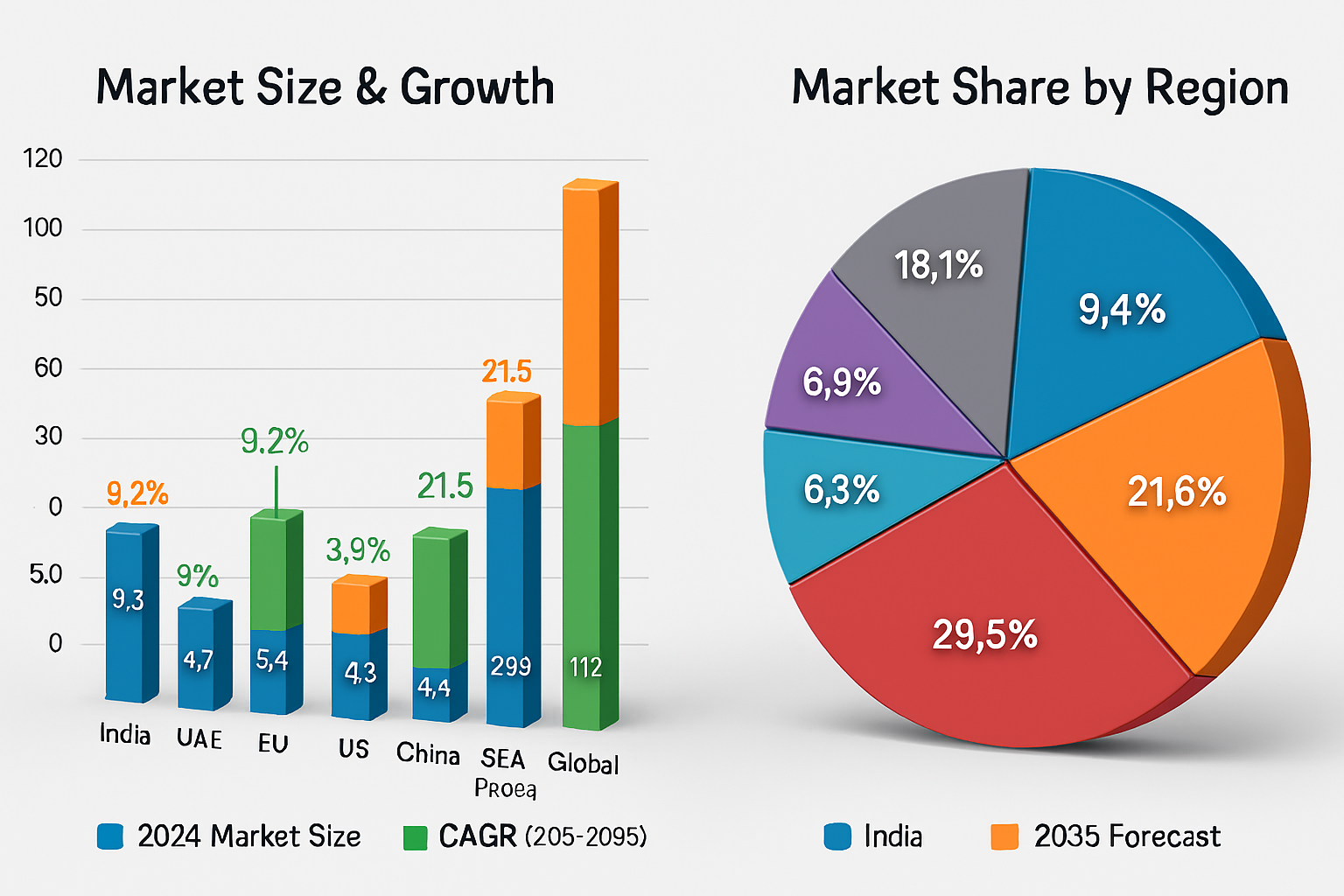

The global market for baby fashion (apparel, footwear, and accessories) for children aged 0-36 months) was estimated to be approximately USD 62 billion in 2024. The sector is expected to grow at a CAGR of ~6.1 per cent between 2025 and 2035 , slated to reach a value of USD 112-115 billion by 2035.

Growth spurs on growth.

Increasing disposable incomes in developing countries (India, China, and Southeast Asia).

The rise of premiumization in the markets of the UAE and the EU.

Greater online penetration, and consumption based on social media (Instagram, TikTok, mom influencers).

Increasing focus on sustainability (organic cotton, eco-friendly dyes).

2035.

Cultural fashion heritage

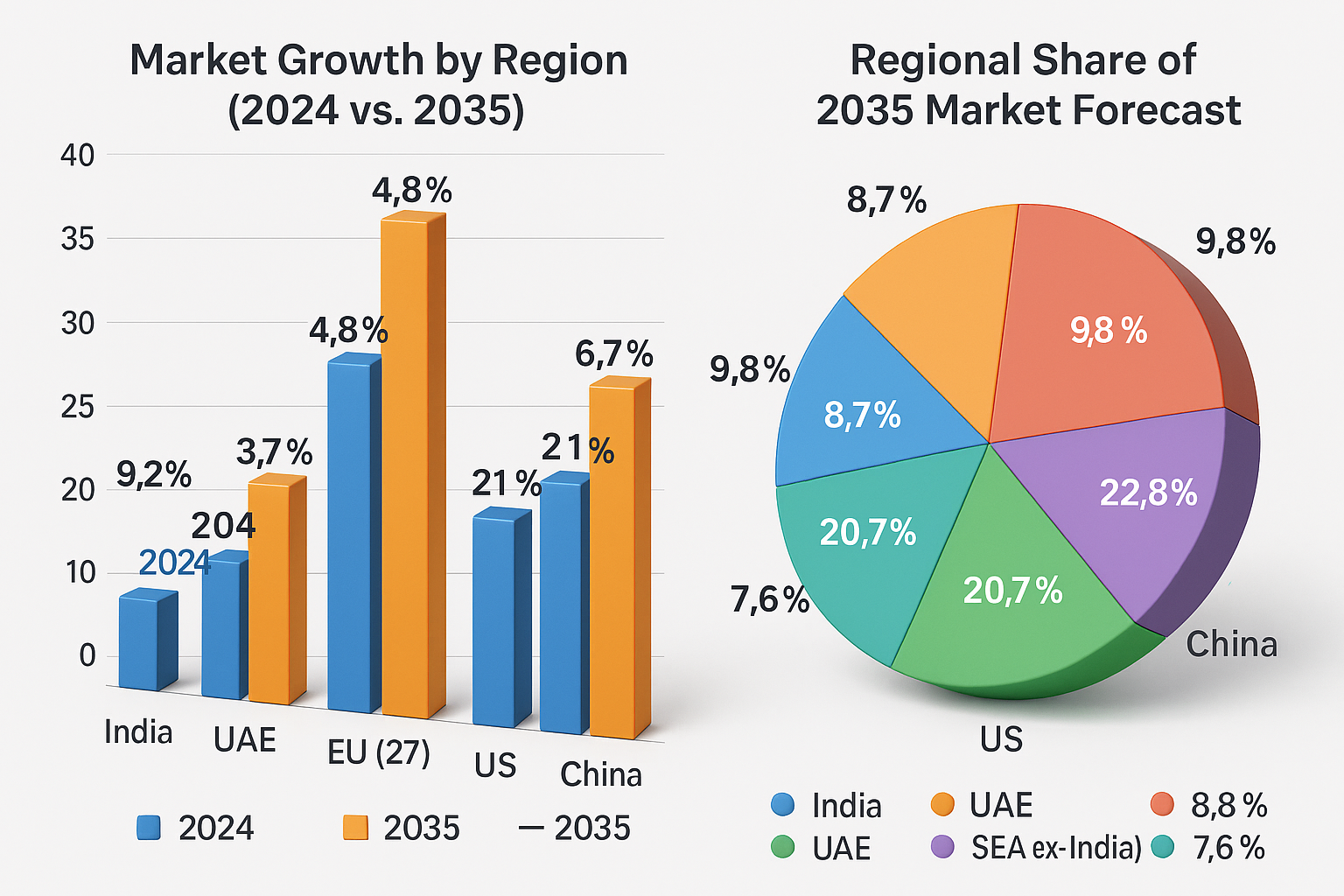

Regional Market Sizing & Growth (2025–2035)

-

Rising middle class

-

Luxury demand

-

Stable demand

-

Digital retail

Historical Growth Context (2015–2024)

- Between 2015–2019, the global baby fashion industry grew steadily at ~4–5% CAGR, driven largely by emerging markets.

- COVID-19 (2020–2021) caused a temporary dip (~–2% decline in 2020), as offline retail stalled.

- Recovery post-2021 has been robust, especially in India, China, and SEA, where online baby fashion retail jumped >20% YoY.

- In the UAE and the EU, luxury baby fashion (brands like Armani Baby, Gucci Kids, Jacadi, Bonpoint) grew faster than the mass market.

Key Trends Shaping Market Size

-

Premiumization & Luxury Babywear

-

Sustainability & Ethical Fashion

-

E-commerce & Omni-channel Acceleration

-

Cultural Influences

Executive Insights

- High-Growth Markets

- Sustainability Focus

- Industry Consolidation

- Luxury Niches

📊 Visualisations (for the report deck):

- Line chart: Global baby fashion market growth (2015–2035).

- Regional CAGR comparison bar chart (India leading, US/EU slower).

- Pie chart: 2035 forecasted regional market share.

10‑Year Market Research Report

(2025–2035) Baby Fashion Industry

-

Rapid e‑commerce

-

Luxury & expat consumption

-

Mature, digital trading

-

Large portion of global market

Key Industry Segments (structure & sizes - qualitative with share guidance)

Segments by age group (typical industry segmentation):

- 0–6 months (newborn): ~30–35% of unit volume (high repeat essentials).

- 6–12 months: ~20–25% (sustained apparel spend).

- 12–36 months (toddler): ~35–45% (higher variety, shoes & playwear).

Segments by price tier (global rough revenue share):

- Mass / Value: 45–55% — high volume, low ASP — dominant in SEA, India (non‑urban).

- Mid‑tier: 30–35% — branded, design‑led essentials (majority of online sales).

- Premium & Luxury: 10–15% — high margin, concentrated in UAE, China urban, EU affluent families.

Product categories (global revenue split, approximate):

- Apparel (bodysuits, outerwear, playwear, sleepwear): 65–70%

- Accessories (hats, bibs, blankets, diapers† coverables): 15–20%

- Footwear & speciality: 10–15%

Distribution channels (trend guidance):

- Online (marketplaces + DTC): 35–50% by 2030 in emerging markets; 40–55% in developed markets (US/EU) depending on brand.

- Offline (brands, speciality, department stores, boutiques): remains important for discovery, premium experience and luxury.

- Omnichannel / hybrid: growing (click‑and‑collect, marketplace + flagship).

Geographical Analysis

High growth, strong online adoption, price sensitivity but rising premium pockets.

Small market, premium & gifting orientation; high per‑capita spend.

Large mature market, sustainability & regulation prioritize organic product lines.

Large mature market with stable demand, strong registry & omnichannel retail.

Rapid premiumization; imported brands perform strongly.

Current Market Offerings

-

Essentials (bodysuits, sleepers)

-

Specialty (organic, hypoallergenic)

-

Fashion/lifestyle lines

-

Accessories & footwear

Gap Analysis

-

Size & fit standardization

-

Lack of accessible certified organic options at mid‑tier price points

-

Limited lifecycle / resale options

-

Sparse product personalization

Identification of Market Opportunities

-

India & SEA premium mass

-

China luxury market

-

UAE luxury & gifting

-

Subscription & recurring revenue models

Risk Analysis & Mitigation Strategies

-

Economic downturn

-

Supply chain disruption

-

Regulatory non‑compliance

-

Greenwashing reputational risk

Share this service:

Leave a comment

Your email address will not be published. Required fields are marked *